The energy research firm estimates that Asia’s thermal consumption could reach 150 million tonnes (Mt) cumulatively by 2030, with nearly half of the increase occurring in 2026 alone. The shift is being driven by an anticipated LNG supply shortfall of 35Mt this year.

Damage to Qatar’s Ras Laffan LNG facility has removed approximately 10.2 million tonnes per annum (Mtpa) of LNG supply to Asia, triggering force majeure declarations and tightening regional gas markets. The resulting supply crunch has pushed the Asia spot LNG price close to three-year highs, leaving gas-dependent economies scrambling for alternative fuel sources.

Rystad Energy estimates that around 90 terawatt-hours (TWh) of power generation will shift directly from gas to coal as utilities seek to compensate for reduced LNG availability. Under a sustained, tight gas market scenario, the firm expects Asia’s incremental coal consumption to increase by nearly 70Mt in 2026, largely through higher utilisation of existing coal-fired power plants.

Following the Iran war, several Northeast Asian governments temporarily relaxed regulatory limits on coal-fired power to bolster energy security, including suspended emissions caps, eased operating-hour restrictions for aging plants, and fast-tracked permits for higher plant utilisation.

This includes Japan, which has temporarily removed a rule limiting coal plants with efficiency below 42 per cent to annual capacity factors of 50 per cent or less, in the fiscal year April 2026–March 2027.

Coal-fired generation has already risen across parts of Asia. In Japan, coal power generation increased 11 per cent in April while gas-fired output fell 13 per cent. Meanwhile, coal imports in South Korea and Japan were more than 50 per cent and 20 per cent higher, respectively, in May compared with a year earlier.

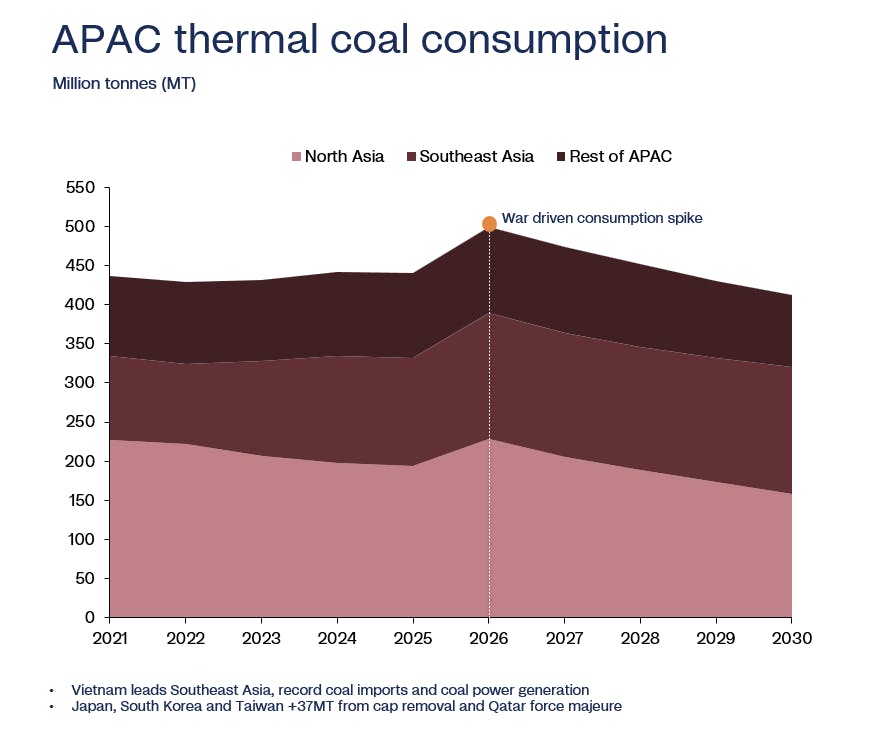

Calculations exclude China and India. Source: Rystad Energy Power Macro Solution, June 2026. Image: Rystad Energy

“What we are seeing is not a coal comeback but a reality check for Asia Pacific’s energy transition. LNG price volatility has shifted costs without reversing the move toward cleaner energy and thermal coal prices have responded to that tightness with cautious buying, stockpiling and a geopolitical risk premium rather than any structural change,” said Tonmit Talukdar, coal research analyst at Rystad Energy.

He said coal is serving as a backup fuel during periods of elevated gas prices and supply disruptions, but the current market response remains more restrained than during the 2022 Russia-Ukraine crisis, when severe gas shortages triggered a sharp spike in global coal demand.

However, stronger coal inventories and record levels of renewable energy deployment in China, India and other major Asian markets have helped prevent a more severe supply squeeze this time.

Talukdar added that until energy storage, grid flexibility, and firm low-carbon generation capacity are sufficiently developed to cover peak demand and periods of intermittency, coal will continue to serve as the system’s fallback.

Rystad Energy also forecasts Newcastle 6000 kcal thermal coal, the benchmark for seaborne coal traded into Northeast Asia, to average around US$125 per tonne in 2026 before easing to US$115 per tonne in 2027 as LNG supplies improve and nuclear power generation increases in the region.

Before the Iran war, coal prices ranged between US$98 and US$115 per tonne, supported by resilient Asian demand. It was then followed by a sharp spike to US$135 per tonne in March 2026 due to the geopolitical crisis and LNG supply shortage.

The largest increases in coal demand are expected in gas-dependent economies. Japan is projected to lead growth, followed by South Korea and Taiwan, where LNG supply disruptions and lower nuclear output are increasing coal consumption. In Southeast Asia, Vietnam, Thailand and the Philippines are also expected to raise coal burn rates to offset tighter gas balances.

China, by contrast, is expected to remain relatively insulated from the shock due to the limited role of gas in its power generation mix, contributing only marginally to additional seaborne coal demand.

Rystad Energy warned that coal demand could climb even further if geopolitical tensions escalate. In a downside scenario involving renewed hostilities, coal demand could increase by approximately 90Mt in 2026 alone, pushing cumulative near-term demand growth to around 190Mt.

Despite the near-term boost in consumption, the firm noted that major coal producers have yet to approve significant new mining projects or substantially extend mine lives, a marked contrast to the period following Russia’s invasion of Ukraine in 2022.